Sometimes I run across articles that make me think about how they relate to my own idea of how to run a financial planning practice. I think about the specific points made, consider how these points apply to me, and then respond appropriately. They make me think and sometimes my thoughts force me to address changes that I might need to consider making or possibly they re-confirm decisions that I have already made. Either way, it’s a win-win, and I become a better advisor.

Alan Roth is a financial advisor from Colorado Springs (Wealth Logic). He has developed a reputation for thinking-outside-the-box and isn’t afraid to ask tough questions or ruffle feathers. His advisory practice is set up to create a financial plan with a fairly simple investment allocation and supply a set of straightforward instructions for the client to follow going forward. It’s a one-and-done deal, and he quips that once completed, the client is encouraged to “fire” him. He charges a premium for this but it is usually quite a bargain compared to being charged a fee based on assets year after year.

Mr. Roth is an accomplished writer as well and publishes articles regularly. Most are succinct reads that often provide a fresh or alternative perspective on old subjects. A recent article of his outlines the ten things he does to differentiate his practice from an otherwise increasingly commoditized profession. Roth champions the hourly fee arrangement as opposed to the popular percentage of Assets-Under-Management (AUM) and states that simple portfolios are typically a better fit for a complex world, especially when it comes to taxes and other more complicated considerations. There are plenty of nuggets here that I find thought-provoking.

For instance, he maintains an anti-sales approach and insists that after a free 20-minute consultation, the client should sleep on it before committing to an engagement no matter how eager they might happen to be at that moment to sign up. His streamlined client acquisition approach is also appealing. He requires each client to fill out an online questionnaire before the 20-minute consult in order to gain a good idea of the client’s current situation and their reason for reaching out. This helps him weed out people who are really not a good fit for his approach and probably won’t really buy-in. All the same, those who fill out that questionnaire still get the free 20-minute consult and his advice on how best to move forward.

Let’s face it. There are probably too many advisors out there earning that typical 1% AUM fee year over year who probably are not really earning it on an annual basis, especially after the client is set up initially. However, my particular belief is that most financial plans are truly a work-in-progress that do need to be monitored on a timely basis and that a good advisor can also serve as a “coach” keeping the client motivated and disciplined over time, especially during periods of market turbulence. I’m comfortable in my vision of keeping fees relatively low but ongoing. However, I do believe in allowing the client to choose another approach (the one and done) if that makes them more comfortable.

Another recent article that caught my attention was written by Dorothy Hinchcliff and published in in the November 2018 issue of FA Magazine. It discusses how advisors can really help those nearing or in retirement by addressing ten important issues.

The 10 issues to discuss are:

1. When and how will a client retire?

2. When should the client start Social Security?

3. How can the client use savings to build a retirement income portfolio?

4. What Medicare choice should the client make?

5. Does the client need to reduce living expenses, and how?

6. Should the client deploy home equity to generate income?

7. How can the client protect against long-term-care expenses?

8. How can clients protect themselves against financial fraud?

9. How can a spouse be protected when the client is gone?

10. Does the client want to plan for a financial legacy?

The articles suggests creating three separate sources for satisfying retirement financial needs:

• Retirement paychecks. These are guaranteed to last the rest of your life, no matter how long you live, and they don’t go down in stock market crashes. Use these to cover your basic living expenses, food, a roof over your head, medical premiums, utilities. Retirement paychecks can come from Social Security, a traditional monthly pension, a low-cost annuity or a reverse mortgage.

• Retirement bonuses. These typically come from invested assets or salaries from working. Use these to cover your discretionary living expenses, like travel, hobbies and gifts for grandchildren. Retirement bonuses can come from systematic withdrawal plans, including the IRS’s required minimum distributions from retirement accounts; interest and dividends from savings; working or self employment; and rental real estate.

• Cash stash. This money covers emergencies so you don’t have to dip into your savings.

A quote from the article: “The secret is paying attention to motivation and inspiration. The strategies are straightforward to understand, but they’ll take discipline and hard work to implement. And that’s where advisors play a key role. To help inspire, and motivate and persist, and to encourage your clients.”

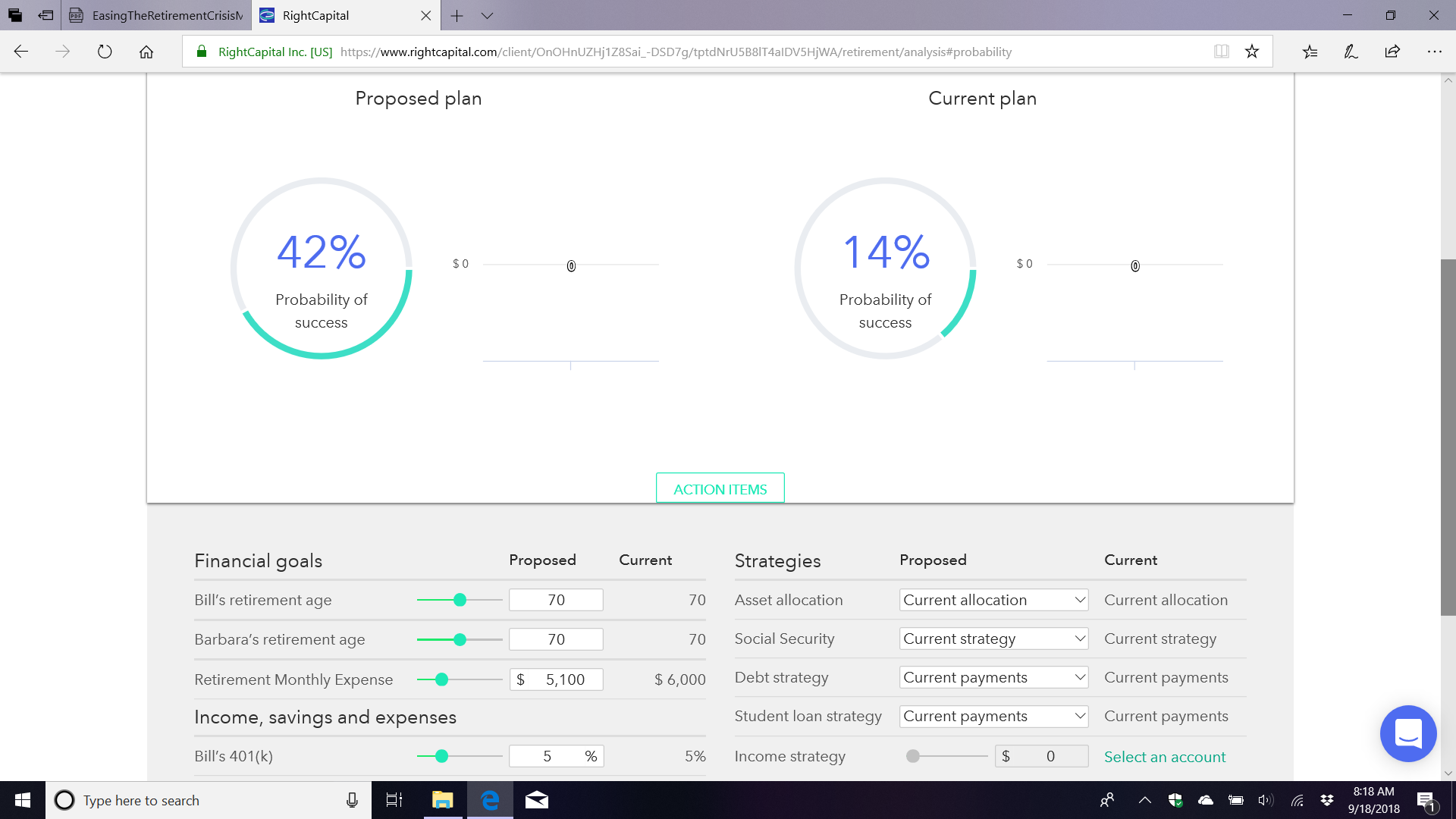

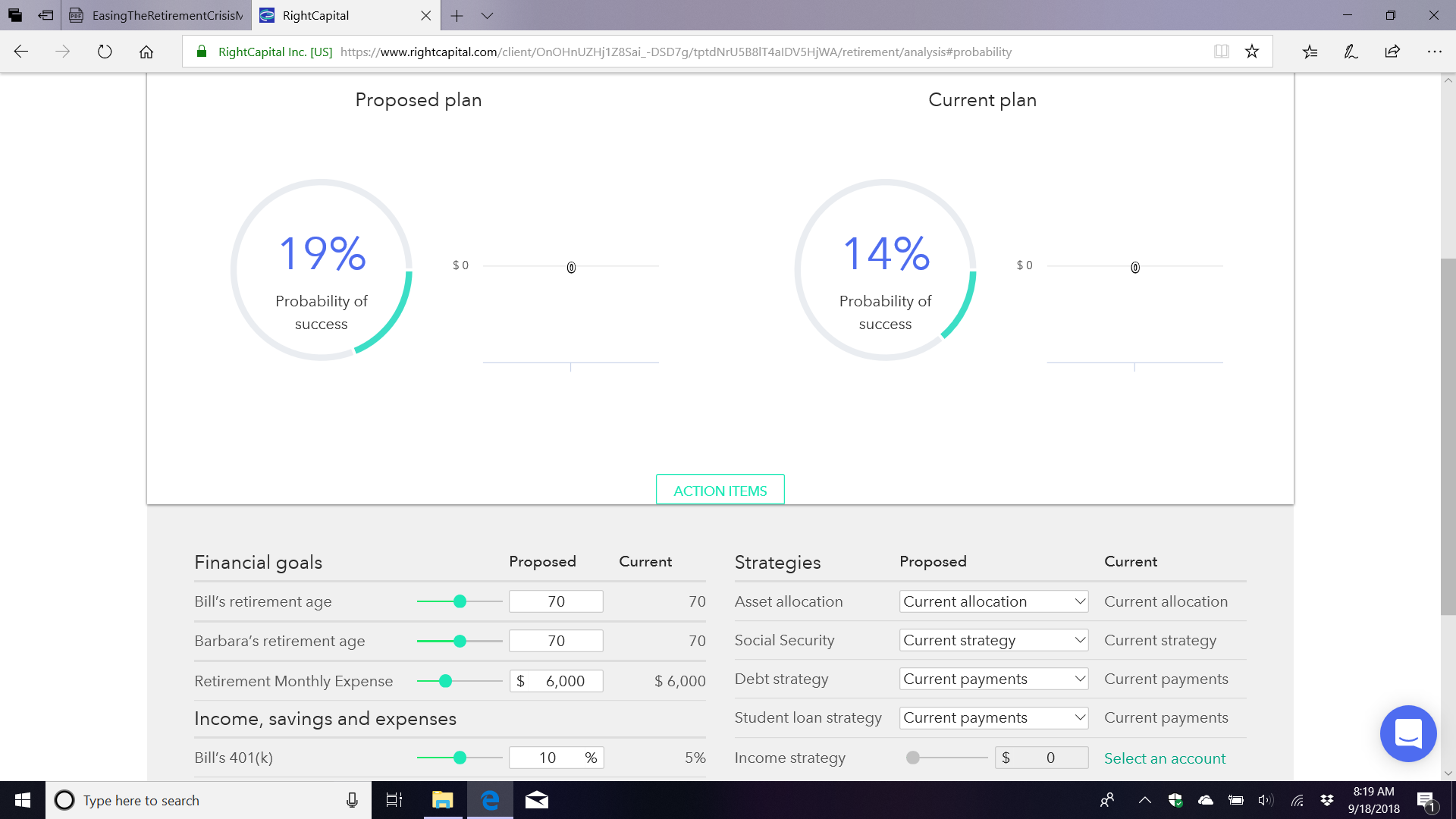

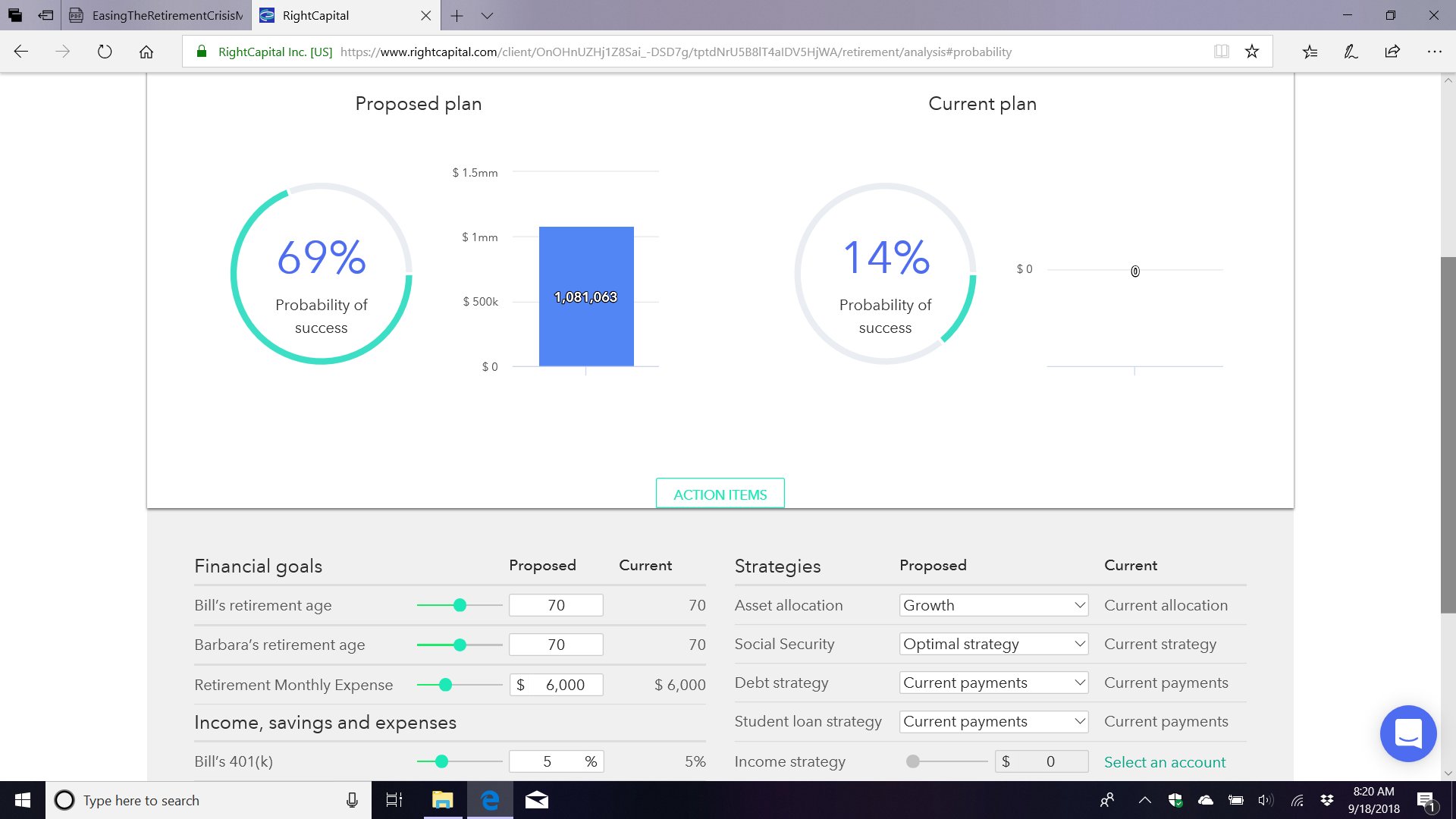

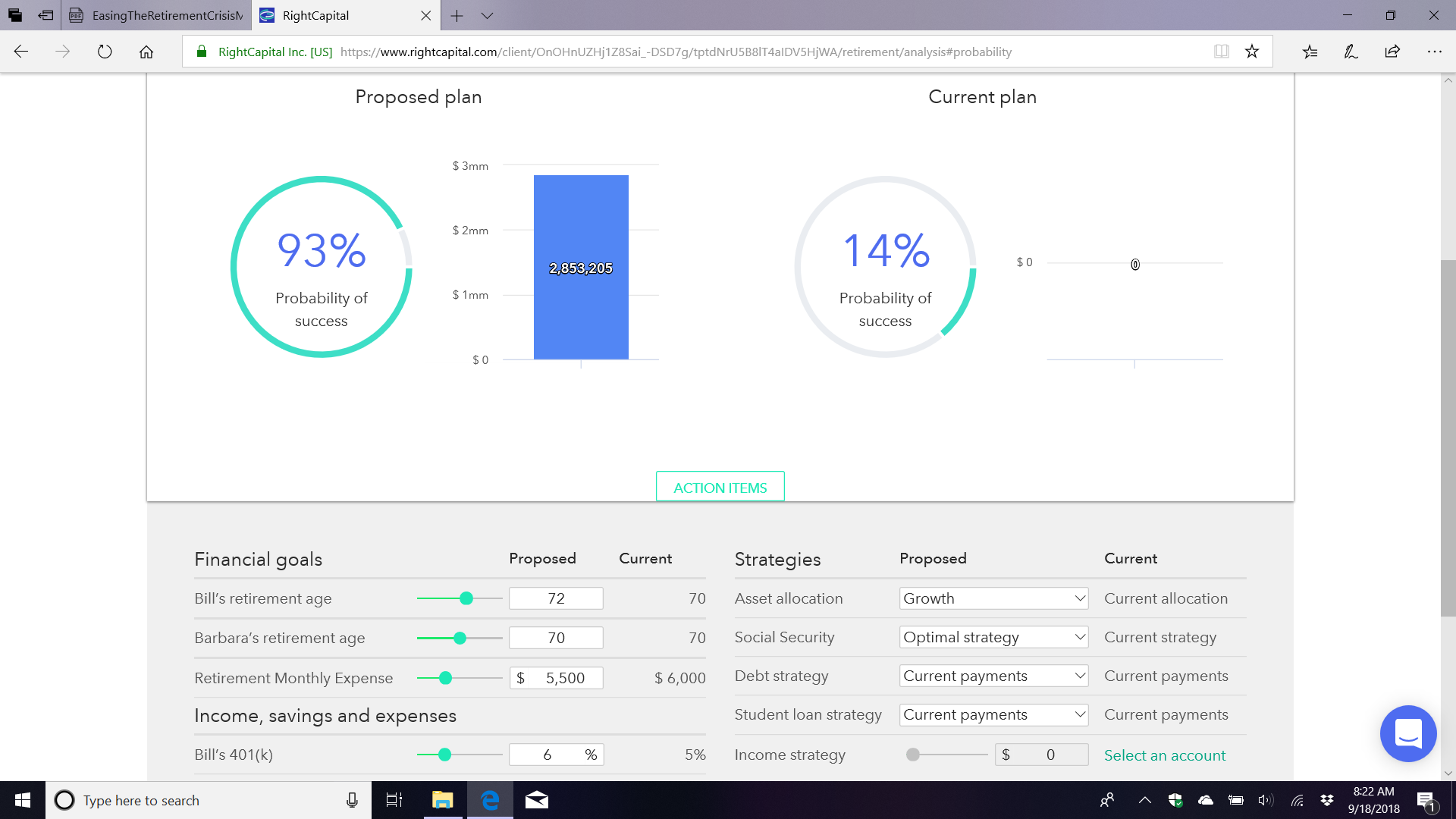

The above ten questions and their respective answers in one way or another form the basis of a strong retirement plan.